Australia’s NEM flips: when power pays consumers

Australia’s NEM flips: when power pays consumers📷 Published: Apr 23, 2026 at 12:05 UTC

- ★Renewables supply 80% of paid demand

- ★South Australia as grid anomaly

- ★Demand shifting from managed to needed

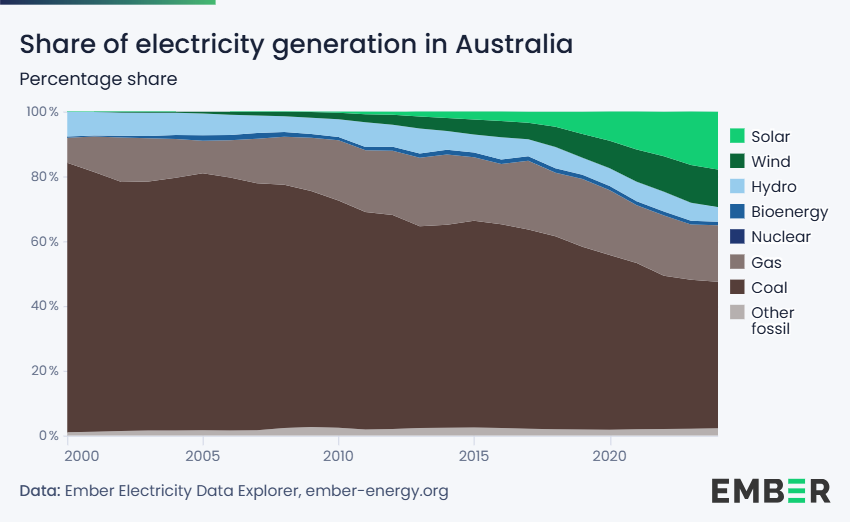

South Australia’s National Electricity Market (NEM) hit an inflection point in Q4 2025: nearly half the time, grid-connected loads were actually paid to consume electricity via spot pricing. The twist? Eight in ten of those episodes came from renewable sources, primarily wind and solar, exposing a fundamental shift from scarcity-driven demand management to abundance-driven demand hunger. Across Australia’s NEM, states with high renewable penetration like South Australia are witnessing negative pricing events not as exceptions but as routine market signals.

This phenomenon, described internally as "growing demand for demand," signals a structural realignment. Where grids once paid to suppress consumption, they now pay to stimulate it—whether through industrial load incentives, residential battery arbitrage, or dynamic pricing schemes. Early data from the Australian Energy Market Operator (AEMO) suggests these negative-price windows are expanding in duration, not just frequency, creating new revenue opportunities for flexible assets.

The demand paradox emerging in ultra-green grids📷 Published: Apr 23, 2026 at 12:05 UTC

The demand paradox emerging in ultra-green grids

The market mechanics behind this are still murky. Speculation points to renewable overbuild outpacing traditional baseload flexibility, but concrete policy levers remain unspecified in official filings. Industry players note that South Australia’s 70%+ renewable penetration creates acute visibility into this trend, though it may not yet reflect national averages. What’s clear is that legacy demand-response programs are being repurposed: from emergency curtailment to strategic consumption reward, a subtle but critical inversion.

For buyers of electricity, the implication is a bifurcated future. Fixed-price contracts lose appeal when spot markets occasionally pay consumers; conversely, exposure to negative pricing becomes a profit center for nimble operators. The question is whether this pattern scales beyond early-adopter regions—or if it’s a canary in the coal mine for larger reliability challenges.

Will other regions replicate South Australia’s negative pricing frequency, or is this a local fluke of renewable timing and grid topology?